( Reading Time: 5 min 48 sec )

The best budget in the world may need a little love and attention to get it healthy as it travels with us through life’s journey. We didn’t create this article to focus on the negative. The purpose was to get us to recognize and avoid the negative things that inspire people to avoid or stop budgeting.

Budgeting is a powerful and effective tool to help us achieve what we want to do with our income. We want to protect it from what would take that power away.

Let’s jump in from 1 to 10, not in any particular order. Please avoid getting caught up in any of these; the goal is to provoke thought and prevent surprises that should not surprise us. Avoiding these is loss prevention.

#1: Unclear Goals

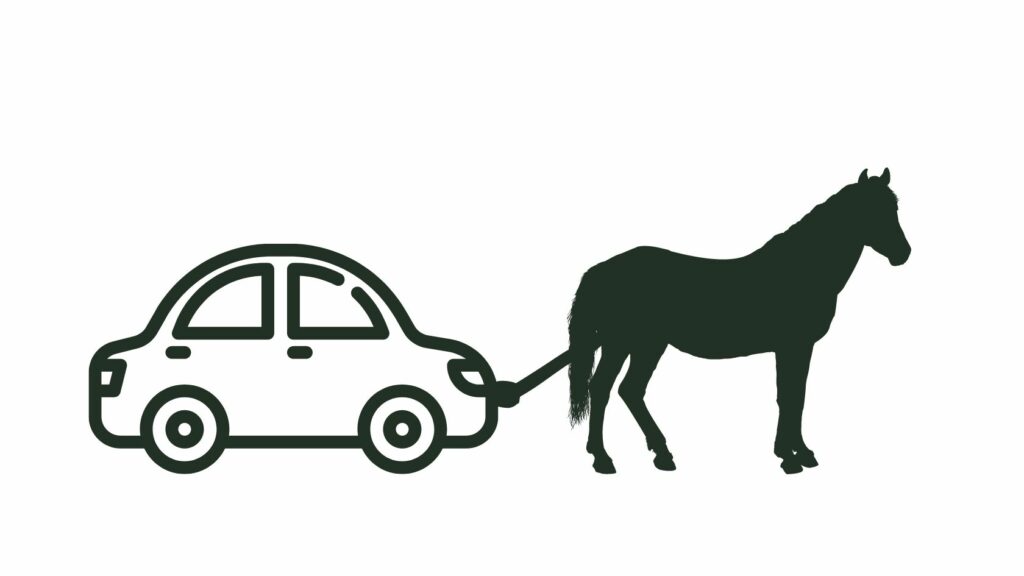

What would the results be if someone, we will call Mary, told a friend, Bob, that they needed a car and would pay them to make one? We all naturally know more detail is required. Without the details, Bob may go off in what seems like a random direction to Mary.

What if Bob returned with a horse-drawn car? Mary stands there looking at it, trying to figure out what to say. Finally, she says, is that a car? Do you expect me to pay for that?

Bob responds, yes, and yes. Here are the advantages of my creation.

- It is safer than modern cars with auto-pilot.

- It can find your way home while you sleep.

- It reduces the weight of the vehicle.

- It has a faster build time.

- Building one costs less; we can sell them together if you like it.

- It has Zero emissions.

- It also saves on insurance.

Budgeting with unclear goals isn’t usually this radical, but it may be just as frustrating over time. Clear goals are essential to long-term budgeting success. If you budget alone or with someone else, the challenges are different, but the need for clear goals is still crucial.

These goals can shift, and the budget can be adjusted.

Bonus: Avoid an overly detailed budget. Making changes becomes too complicated with too much detail. Then, you will either find yourself adjusting your goals to align with your budget or putting the budget aside to pursue the goals.

#2: Pretend Plans

Have you heard of the 50-30-20 rule? The suggestion is to take fifty percent of the income towards needs, thirty percent towards wants, and twenty percent towards savings. This rule may be a good starting budgeting guide. What it is not is a reasonable budget. If this is your first budget, or your current budget is a disaster, this would be a good pivot for one cycle.

Your plan must work with your situation, income, and expenses. There are many reasons for creating fake budgets. Perhaps you don’t want to budget. Budgeting reminds you of what you cannot do. You are using your friend’s budget because they like it, so it must be good for you also.

A budget must reflect your income and your expenses. The budget needs to cover your regular and irregular expenses. It has to be a real plan, or you might be wasting time budgeting. You don’t have to get everything right the first time or every time. What you do need is to learn to make a budget that is resilient and agile.

#3: Ignoring Execution

We make budgets to guide our income to deliver particular results. If we don’t spend according to the plan, we are not likely to get the results of our plans. Plans can be adjusted by moving money from one budget category to another.

When we spend the money with a mental plan to adjust the numbers later, it usually doesn’t happen. It is best to adjust the numbers first. If you use a program like YNAB, post-adjustment is less risky. Adjustments after the fact will feel and think differently than adjustments we make before spending.

#4: Misunderstanding the responsibilities of a budget

One reason people give for not budgeting is that it wasn’t working for them. We ask them to explain, and different stories have a common theme.

Some people look to their budget to find a way to give them more than their income can deliver. Buying bigger or more things in this struggle is solved with a more significant income. The budget is not responsible for helping us spend the same dollars twice or to magically make the income bigger than when we received it. The job of the budget is to choose how to spend our income on our goals best. That is what makes budgets incredible, not frustrating.

Others look at their budgets to solve the unexpected challenges of life. They may expect a category called emergency fund to prevent any unexpected events that total more than they have in this fund. These events are unplanned, but we can predictably estimate buffer funds for these events. If we can save enough, that is because we have enough income to do it without other goals. If we are not, it is not a shortcoming of the budget.

Budgets help us understand what type or how big an emergency we can be prepared to respond to financially. Understanding helps us be sure about this security buffer. Knowing is the benefit of budgeting.

If we spend our budgets on personal things so much that our priorities and long-term goals are neglected, that is the budgeter’s call. Budgets are faithful and compliant to any choice you make. Who can get upset with this level of cooperation?

#5: Fantasy Budgeting / Spending

Lifestyle or in-the-moment spending beyond what works towards our goals or in ways that exceed our income will make your budget unfriendly. You look at your bank accounts, credit cards, and other resources, and more must be left for your core needs.

The solution here is to realize the budget can be adjusted. Correct the budget by determining where this money came from and what you said no to when you said yes to other things. It is not a fun job, but it is powerful. The training of our mental muscles and character is powerful when we ask what we said no to each time we practice fantasy spending. It is far more powerful long-term than shopping or restaurant therapy.

#6: Lack of Income

We did mention this one above. If our financial needs exceed our income, we might want to dedicate some of our budget to pursuing more income. This should never be gambling. We want to invest in our future, not risk it.

#7: Impersonal Plans

Budgets must match our needs, goals, and income, as we just cited. Our similar friends may have similar budgets, but the differences are important. Living on someone else’s budget may be like eating someone else’s menu plan. Your budget must match your needs and wants within the available income to fund it.

#8: Outdated Plans

Just like you are different from your friends, you are different from you of yesterday and tomorrow. You change, the economy changes, income changes and seasons change. Reworking the budget keeps the benefit of budgeting in play.

#9: Despair, Conflict

Our emotional state will often have more control over our budget than math. Poor emotions tend to inspire poor math. Poor math, when it comes to budgeting and spending, tends to inspire poor emotions. Can you see a downward spiral is possible as these feed each other?

We also have others in our lives. Other people include children, parents, neighbors, spouses, bosses, and any other relationship we focus on. Learning interpersonal skills impacts the emotions that impact our budgeting math.

#10: Poor Vision

A lack of vision prevents us from being prepared for opportunities and challenges. When we look at the past, we can apologize and gain new insight, but we cannot go back and live it differently. The past has passed. Our vision of the path should be meekness, whether we lived it well or poorly.

The future should always be an investment without forgetting to live with meaning today. Living today with meaning should always be exercised with awareness of how it impacts the future.

If we do this, our vision will be much clearer. Our past will not gain extra power to hold us back. Our future will be enhanced by our choices today.

Summary

We recognize that some of these are related. Yet, we have found in coaching that close. Like a good budget, you can modify the list to meet your needs and perspective. These are our numbers, and they work for us. Adjust and apply so you get more traction, or in this case, avoid more brittle points in your budgets.